What LiDAR Mapping Has to Do With Your Flood Insurance Bill

Your flood insurance premium went up. Your property never flooded. And nobody explained why. The answer is sitting in a FEMA database built on LiDAR elevation data, and most homeowners have never heard of it.

This article explains how LiDAR mapping connects to flood zone decisions, why those decisions directly affect what you pay for insurance, and what a licensed surveyor can do when the data gets it wrong.

How FEMA Decides Your Flood Zone

FEMA publishes Flood Insurance Rate Maps to show which properties carry flood risk. Lenders use these maps to decide whether flood insurance is required. Insurance companies use them to set your premium.

For decades, those maps were built on outdated methods. Some hadn’t been updated in 40 years. They missed how water actually moves across flat, low-lying terrain where elevation changes by inches, not feet.

That changed when FEMA began using LiDAR data to rebuild its flood maps from scratch.

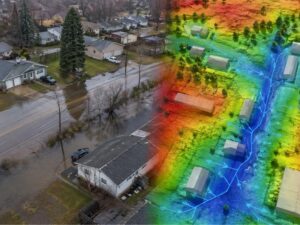

What LiDAR Mapping Actually Does

LiDAR stands for Light Detection and Ranging. A plane or drone flies over an area and fires millions of laser pulses at the ground. Each pulse bounces back and records an elevation point. The result is a three-dimensional model of the terrain with centimeter-level accuracy.

For flood modeling, that level of detail matters. A two-foot difference in ground elevation can determine whether a property sits inside or outside a flood zone. Old survey methods couldn’t capture that consistently across large areas. LiDAR can.

FEMA’s updated flood maps for South Florida were built on this data. Engineers used the LiDAR elevation model to calculate where water goes during a major storm, how far it spreads, and which properties fall inside the projected flood boundary.

That boundary is what sets your flood zone designation. And your flood zone designation is what sets your premium.

Why So Many Properties Got Reclassified

When FEMA updated Broward County’s flood maps using LiDAR elevation data, 88,000 properties were moved into higher-risk flood zones. Many of those homeowners had never been in a flood zone before. Some had owned their properties for decades without a flood insurance requirement.

The maps changed because the data got better. LiDAR revealed elevation differences that older methods missed. Properties that looked safe on a 1980s paper map turned out to sit at elevations where water accumulates during heavy rainfall events.

That’s not a billing error. It’s a more accurate picture of actual terrain. The problem is that LiDAR data, while precise, still has limits. It measures the surface. It doesn’t account for drainage infrastructure, canal systems, or permeable ground that absorbs water before it reaches a structure. A property can appear to be in a flood zone on a LiDAR-based model and still drain well in practice.

When that happens, a licensed surveyor can document the discrepancy.

What a Surveyor Can Do About a Wrong Designation

If your property was placed in a flood zone you believe is inaccurate, you have options. FEMA allows property owners to submit a Letter of Map Amendment (LOMA) to challenge a flood zone designation. A LOMA requires a licensed surveyor to release an elevation certificate of your property’s lowest adjacent grade relative to the Base Flood Elevation shown on the FEMA map.

If the surveyor’s certified measurements show your property sits above the Base Flood Elevation, FEMA can remove it from the high-risk zone. That removal typically drops or eliminates the flood insurance requirement tied to a federally backed mortgage.

The LiDAR model gets FEMA close. A licensed surveyor with ground-level measurements gets it right.

This is not a minor distinction. The difference between an AE flood zone designation and an X zone can mean thousands of dollars per year in insurance premiums.

How to Know If Your Designation Might Be Wrong

Not every reclassification is an error. But some are, and the signs are worth checking.

Your designation may be worth reviewing if:

- Your property sits noticeably higher than neighboring lots that are not in a flood zone

- You’ve never had water intrusion despite being in a high-risk zone for years

- Your lot was recently reclassified despite no physical changes to the property

- Your neighbor’s identical lot carries a different flood zone designation

A licensed surveyor can review the FEMA panel covering your property, compare it against a current elevation measurement, and tell you whether a LOMA filing makes sense. That review costs far less than a year’s worth of flood insurance premiums on a property that may not need the coverage.

Frequently Asked Questions

What is LiDAR mapping and how does it affect flood insurance?

LiDAR mapping uses laser pulses to measure ground elevation with high accuracy. FEMA uses LiDAR data to build flood maps that determine which properties fall in high-risk flood zones. If your property is in a designated flood zone, your lender may require flood insurance, and your premium is based on that zone classification.

Why did my flood zone designation change if my property never flooded?

FEMA updated its flood maps using more accurate LiDAR elevation data. The new maps reflect terrain more precisely than older methods. Some properties that appeared safe on older maps now sit within the projected flood boundary based on current elevation modeling.

Can I challenge my FEMA flood zone designation?

Yes. You can apply for a Letter of Map Amendment (LOMA) through FEMA. The process requires a licensed land surveyor to certify your property’s elevation. If the certified elevation shows your lowest adjacent grade sits above the Base Flood Elevation, FEMA may remove your property from the high-risk zone.

How accurate is LiDAR flood mapping?

LiDAR achieves vertical accuracy of plus or minus 10 to 15 centimeters under standard collection conditions. That accuracy is sufficient for large-area flood modeling but may not reflect site-specific drainage conditions, infrastructure, or fill. A ground-level survey by a licensed surveyor provides the precise elevation data needed to challenge a designation.

How much can removing a flood zone designation save on insurance?

Annual savings vary by property value and insurer. Homeowners removed from a Special Flood Hazard Area through a LOMA typically eliminate the mandatory flood insurance requirement tied to a federally backed mortgage. For many property owners, that represents savings of $1,000 to $3,000 or more per year.

For a free land surveying quote, call us at (954) 519-7803 or send us a message by going here.

Posted in land surveying, land surveyor |